If you are a retiree, a downsizer, or just someone chasing better weather and a lower tax bill, you have probably typed “utah vs arizona cost of living” into a search bar more than once. And you have probably gotten back a vague blurb: cost-of-living indexes, a percentage here, a “both are affordable” there. What those summaries almost never tell you is the stuff that actually hits your wallet when you own a home in one state versus the other. So let’s get specific.

This is a side-by-side look at how income and property taxes really work in each state, what you pay at closing when neither state charges a transfer tax, how the climate quietly shapes your utility and maintenance bills, and how the home-buying paperwork differs once you cross the state line. None of this is tax or legal advice, but it should give you concrete questions to ask before you sign anything.

How Income and Property Taxes Compare

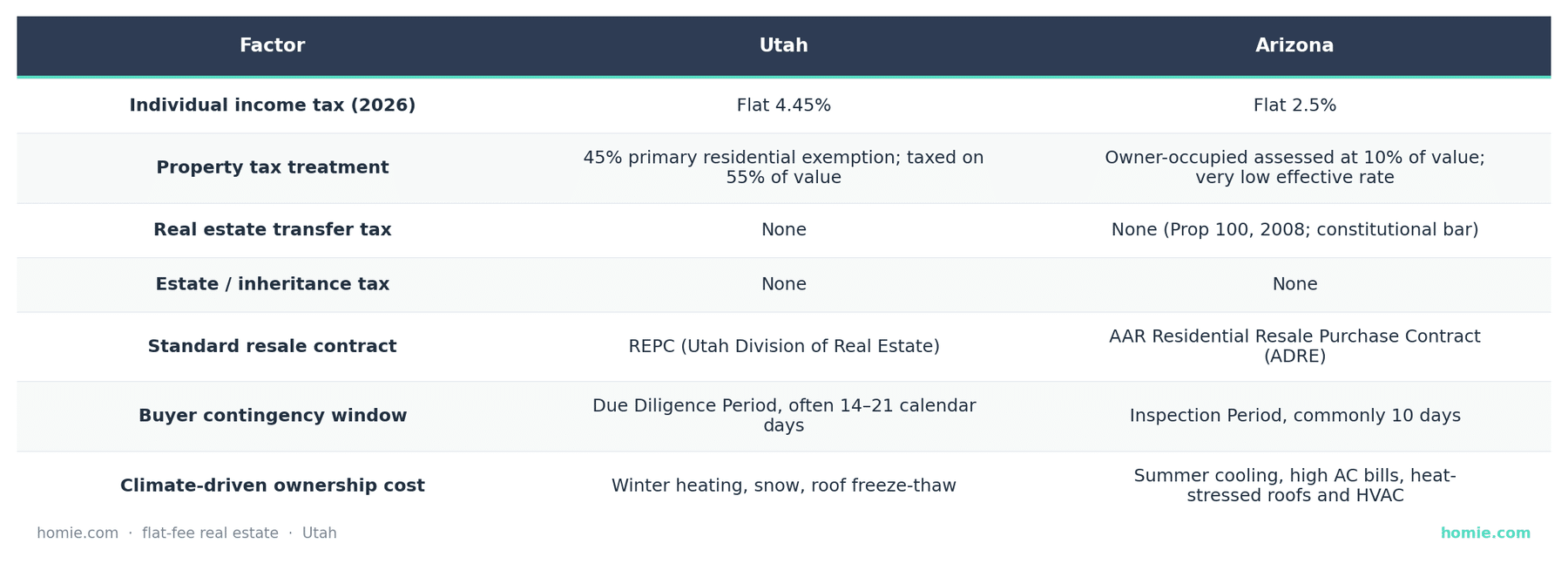

Both states keep things simple on income tax, and both lean toward flat rates rather than the stacked brackets you see elsewhere. For the 2026 tax year, Utah uses a flat individual income tax rate of 4.45%, the latest in a string of small annual cuts. Arizona sits lower, at a flat 2.5%, one of the lowest flat rates in the country. Neither state taxes Social Security in the way some others do, which matters a lot if you are retiring on a fixed income. Property tax is where the two states diverge in mechanics, even if the end numbers land in a similar neighborhood.

Utah gives owner-occupants a primary residential exemption: 45% of your home’s fair market value is exempted, so you are taxed on only 55% of it. To qualify, the home generally has to be your primary residence for at least 183 consecutive days a year, and you only get the exemption on one home. A vacation cabin or a second home does not count. Arizona handles it through assessment ratios. Owner-occupied homes fall into a property class assessed at 10% of the home’s value, and the state’s effective property tax rate is among the lowest in the nation, in the neighborhood of 0.6%.

Arizona also has no state estate tax and no inheritance tax, which is part of why it shows up so often on retiree-friendly lists. The practical takeaway: run your specific numbers for the specific county and home, because two homes at the same price can carry very different bills depending on local rates and which exemption or ratio applies.

What You Actually Pay at Closing

Here is a pleasant surprise for anyone moving from a state like Pennsylvania or New York: neither Utah nor Arizona charges a real estate transfer tax. In Arizona, that is locked in fairly tightly. Proposition 100, passed by voters in 2008, amended the state constitution to prohibit new transfer taxes on the sale of property, so it would take another constitutional amendment to change it. Utah simply does not levy one at the state or local level. That does not mean closing is free, of course. It just means the costs you do see are the ordinary ones. In both states you can expect recording fees, title and escrow charges, lender fees, and prorated property taxes that get split between buyer and seller based on the calendar.

Utah recording fees are modest, often around $40 per document. Arizona requires an Affidavit of Property Value to be recorded with most transfers under A.R.S. 11-1134, which carries a small filing fee and documents the sale price for the assessor. As a rough guide, total buyer closing costs in either state commonly run a few percent of the purchase price, though the line items vary by lender and title company.

How Climate Shapes the Cost of Owning

This is the category the generic cost-of-living calculators are worst at, because they average everything into one number and lose the seasonal swing entirely. The two states stress a home in almost opposite ways. In Utah, the challenge is winter. You are paying to heat the house through cold months, and along the Wasatch Front you are also dealing with snow load on the roof, freeze-thaw cycles, and the occasional burst-pipe risk if a home is not properly insulated. Heating with natural gas tends to keep Utah winter bills reasonable, and summers are warm but generally dry and shorter, so cooling is less punishing.

In Arizona, the challenge is the opposite and arguably more expensive. Phoenix-area summers regularly push past 110 degrees, and air conditioning runs hard for months. It is common for a roughly 2,000-square-foot Phoenix home to see summer electric bills in the $300 to $450 range during the hottest stretch, far above what most Utah homes pay in any single month. That sustained heat is also tough on roofs, HVAC systems, and exterior finishes, so budget for a hardworking AC unit and the maintenance that comes with it. The flip side: Arizona winters are mild, so your heating costs are minimal. Think of it as paying your weather tax in July instead of January.

Contracts and Process for a Cross-State Buyer

If you have bought a home in one of these states before, do not assume the other works the same way. The forms, the terminology, and the timelines are different, and the agency that oversees the whole thing is different too. In Utah, most resale purchases use the REPC, the Real Estate Purchase Contract, overseen by the Utah Division of Real Estate under the Utah Code. The key buyer-protection window is called the Due Diligence Period, often 14 days by default and sometimes 21 for new construction or homes needing septic or well inspections. Those are calendar days, so weekends count, and during that window a buyer can typically inspect, review documents, and cancel while keeping their earnest money if something does not check out. Listings flow through the Wasatch Front MLS.

In Arizona, resale deals generally run on the AAR Residential Resale Real Estate Purchase Contract, with the Arizona Department of Real Estate (ADRE) regulating agents under the Arizona Revised Statutes (A.R.S.). The comparable window is the Inspection Period, commonly 10 days after contract acceptance unless the parties agree otherwise. During that period the buyer can deliver a notice of disapproved items, ask the seller to address them, or cancel. Listings run through ARMLS. Same goal as Utah’s Due Diligence Period, shorter clock, different name and form, so do not let the vocabulary trip you up.

Utah vs. Arizona at a Glance

Frequently Asked Questions

Is it cheaper to own a home in Utah or Arizona in 2026?

It depends more on the specific home, county, and your situation than on the state. Arizona has a lower flat income tax (2.5% vs. Utah’s 4.45%) and very low effective property tax rates, while Utah’s primary residential exemption meaningfully lowers what owner-occupants are taxed on. The biggest hidden swing is utilities: Arizona’s summer cooling bills can dwarf Utah’s, while Utah’s winter heating is usually modest. Add up taxes plus your expected utility pattern for the actual home, not the statewide average.

Does Utah or Arizona charge a real estate transfer tax?

Neither one does. Arizona prohibits transfer taxes through Proposition 100, a 2008 voter-approved constitutional amendment. Utah does not impose a transfer tax at the state or local level. You will still pay ordinary closing costs like recording fees, title and escrow charges, and prorated property taxes.

What is the difference between Utah’s Due Diligence Period and Arizona’s Inspection Period?

They serve the same purpose, a window to inspect and back out, but they differ in name, length, and form. Utah’s REPC uses a Due Diligence Period, frequently 14 to 21 calendar days. Arizona’s AAR contract uses an Inspection Period, commonly 10 days after acceptance. Both let a buyer raise concerns or cancel, but the Arizona clock is usually shorter, so plan your inspections accordingly.

How does Utah’s primary residential exemption work?

If the home is your primary residence (generally occupied at least 183 consecutive days a year), Utah exempts 45% of its fair market value from property tax, so you are taxed on 55%. You can only claim it on one home, and second homes, cabins, and short-term rentals do not qualify. You typically file a declaration with the county assessor to claim or maintain it.

Are both states good for retirees on a fixed income?

Both are frequently cited as retiree-friendly. Arizona has no estate or inheritance tax, a low flat income tax, and low property tax rates, with the trade-off of high summer cooling costs. Utah offers a lower-taxed slice of value on a primary residence and milder summers, with the trade-off of real winters. Confirm how each state treats your specific retirement income with a tax professional before deciding.

Which forms and agencies should a cross-state buyer learn first?

In Utah, learn the REPC and the Utah Division of Real Estate, and know that listings run through the Wasatch Front MLS. In Arizona, learn the AAR Residential Resale Real Estate Purchase Contract and the Arizona Department of Real Estate (ADRE), with listings through ARMLS. Keeping the two states’ forms and timelines straight is the single biggest adjustment for buyers crossing the line.

A quick note from us: we are Homie, a brokerage licensed in both Utah and Arizona, so we end up fielding the “which state should I buy in” question a lot. We wrote this to be genuinely useful no matter where you land, and if you want to dig deeper into the buying process you can start at homie.com/buy. One honest caveat: tax rules and rates change, so confirm the current details with each state’s revenue department and a tax pro before you make a move. This is educational, not legal or tax advice.

— The Homie Team

- Utah State Tax Commission, Primary Residential Exemption

- Tax Foundation, 2026 Utah Tax Rates & Rankings

- Tax Foundation, 2026 Arizona Tax Rates & Rankings

- Arizona Department of Revenue, Property Tax FAQs

- Arizona Department of Revenue, Affidavit of Property Value

- Arizona Revised Statutes 11-1134, Exemptions

- Wikipedia, 2010 Arizona Proposition 100 (transfer tax bar)

- Arizona Association of REALTORS, Contract Series (Inspection Period)

- Aristotle Air, Average Arizona Summer Electric Bill

- r/Phoenix relocation discussions

- r/SaltLakeCity relocation discussions

*All brokerage fees, including listing and buyer agent compensation, are fully negotiable and determined solely by the seller and service provider.

*Flat-fee pricing and service availability may vary by location and are subject to change over time. Verify current pricing before listing.

*Past performance is not indicative of future results.

*Examples and potential savings are for illustrative purposes only.