National rent-versus-buy calculators run on national inputs, so they miss what makes Utah’s answer different: high price-to-rent ratios, a long history of fast appreciation, and Wasatch Front rents that have not kept pace with prices. A relocator deciding whether to buy or rent in Salt Lake, Utah, Davis, or Weber County needs the local math, not the average of fifty states. This article shows how to read the price-to-rent ratio for each county, works a break-even example with current Utah numbers, lays out the costs each side adds, and identifies who is better off waiting. Figures below are illustrative and drawn from the sources at the end. Verify current rents and prices before you decide.

Is it cheaper to rent or buy in Utah in 2026?

In most of the Wasatch Front in 2026, renting carries the lower monthly cost, while buying builds equity and hedges against future rent increases. With median prices well above $500,000 in Salt Lake County and one-bedroom rents near $1,450, the monthly math favors renting in the short term, and the case for buying rests on how long you will stay and whether prices keep rising. There is no single answer for the whole state. The right call depends on your county, your timeline, and what you would do with the cash you are not spending on a down payment.

How do you read the price-to-rent ratio for a Utah county?

The price-to-rent ratio is the median home price divided by the median annual rent. A higher number means buying is relatively expensive compared with renting; a lower number means buying is relatively cheap.

- Ratio under 15: buying is usually favorable.

- Ratio 16 to 20: mixed; depends on your timeline and the costs below.

- Ratio over 21: renting is often cheaper month to month, and buying leans on appreciation to win.

Salt Lake County sits well into the high range in 2026, with a median sale price around $563,000 and overall rents that put the ratio firmly in renting-favored territory. Utah and Davis counties run similarly high, while Weber County tends to be more affordable on both sides, which can pull its ratio down toward the mixed range. Pull current figures from the Redfin Utah market page and a rent source before you apply this to your own county.

What does the break-even math look like with current Utah numbers?

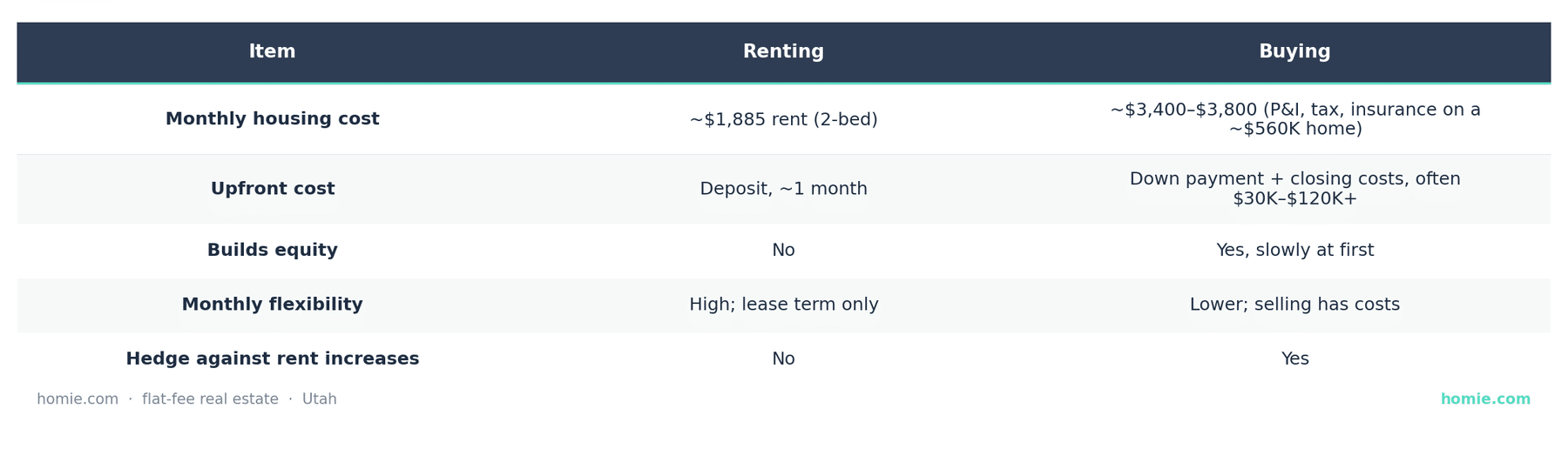

Here is a worked, illustrative example for a Salt Lake County household comparing a two-bedroom rental against buying a similar home. Numbers are approximations for 2026 and should be verified.

At those numbers the renter spends far less per month, and the buyer is betting that appreciation plus equity plus the rent hedge will overtake that gap over time. The break-even point, where buying pulls ahead of renting, commonly lands somewhere in the range of five to seven years in a high price-to-rent market like this, and sooner if prices rise quickly or rents jump. Stay shorter than your break-even and renting usually wins; stay longer and buying usually does. A 30-year fixed mortgage in Utah was hovering near 6% in early 2026, which is the single biggest input in the buying column. Re-run the example with the actual rate you would get, because a one-point move changes the monthly payment materially.

What costs does each side add that the sticker numbers hide?

The headline of rent versus mortgage payment is not the real comparison. Each side carries costs the other does not. Owners add property tax, homeowner’s insurance, any HOA dues, maintenance and repairs (a common rule of thumb is around 1% of the home’s value per year), and the opportunity cost of the down payment sitting in the home instead of invested. Renters skip all of those but get no equity and no protection from the next rent increase, and they carry renter’s insurance and the risk of moving when a lease ends or a landlord sells. When you compare honestly, you put the full owner cost against the full renter cost, including what the down payment could have earned elsewhere. That opportunity cost is the line most calculators understate and the one that matters most for a financially disciplined renter who would invest the difference.

Who should rent longer in 2026, and who is positioned to buy?

The decision tends to sort by timeline and stability more than by income. Rent longer if you might move within a few years, your job or location is unsettled, you are still building a down payment or paying down high-interest debt, or you would invest the monthly savings rather than spend them. In a high price-to-rent market, a short stay rarely clears the transaction costs of buying and selling. Lean toward buying if you plan to stay past your break-even horizon, you value stability and the ability to modify the home, you have a down payment that will not strand your emergency fund, and you want a hedge against Utah’s history of rising rents. Buying is a long-game move here in 2026, not a short-term cost saver.

How does the cost of selling factor in later?

If you buy, plan for the cost of selling when you eventually move, because it affects your break-even. Selling costs include listing-side and buyer-agent compensation, which after the 2024 NAR settlement are negotiated separately and are fully negotiable. Some traditional commission structures may total around 5 to 6 percent, though commissions vary by brokerage and agreement. On a $560,000 home, an illustrative 3 percent listing-side commission rate would be $16,800 (illustrative only; rates vary and are negotiable). Flat-fee listing models replace that percentage with a single fixed fee regardless of sale price, which changes the resale-cost line in your buy-versus-rent math. Buyer-agent compensation is independently negotiable and may vary based on market conditions and buyer representation agreements. Current pricing for Homie’s flat-fee listing is at homie.com/sell.

Frequently Asked Questions

Is renting throwing money away in Utah?

Not necessarily. Renting buys flexibility and avoids maintenance, property tax, and transaction costs. In a high price-to-rent market like the Wasatch Front, a renter who invests the monthly difference can come out ahead of a buyer who sells before break-even.

What is a good price-to-rent ratio for buying in Utah?

Under about 15 generally favors buying, 16 to 20 is mixed, and over 21 leans toward renting month to month. Much of the Wasatch Front sits in the higher range in 2026, so buying there relies more on appreciation and a longer hold.

How long do you have to stay in a Utah home to break even on buying?

In a high price-to-rent market it commonly takes five to seven years for buying to overtake renting, depending on your mortgage rate, price growth, and selling costs. Run your own numbers; a faster-rising market shortens it.

What is the median rent in Salt Lake City in 2026?

Reported averages in 2026 ran roughly $1,400 to $1,600 for a typical apartment, with two-bedroom units in Salt Lake County closer to $1,885. Rents vary widely by neighborhood and unit type, so check a current source for your area.

Will home prices in Utah keep rising?

No one can promise that, and past performance is not indicative of future results. Utah has a long history of appreciation driven by population growth and tight supply, but the buy-versus-rent decision should not assume a specific future rate of price growth.

That’s the break-even picture for the Wasatch Front in 2026. If you’re relocating to Utah and leaning toward buying, homie.com/buy is where we work, and we’d rather you run the math than rush it. Verify current rents, prices, and rates before you decide, because all three move and the answer moves with them.

— The Homie Team

- Redfin Utah Housing Market

- Zillow Salt Lake City Home Values

- Zillow Rental Manager, Salt Lake City rent trends

- HUD Fair Market Rents

- Kem C. Gardner Policy Institute, Utah housing data

*All brokerage fees, including listing and buyer agent compensation, are fully negotiable and determined solely by the seller and service provider. *Flat-fee pricing and service availability may vary by location and are subject to change over time. Verify current pricing before listing. *Past performance is not indicative of future results. *Examples and potential savings are for illustrative purposes only.