For a first-time buyer along the Wasatch Front, the choice between a condo, a townhome, and a single-family house is often the first real fork in the road, and it shapes the budget more than the paint color ever will. The three look similar in a listing feed, but they differ in what you actually own, how they are financed, what an HOA can charge you, and how they hold value over time. Generic comparisons explain the basic types; this one adds what Utah’s Community Association Act, condo financing rules, and entry-level pricing mean for the decision here.

What do you actually own in each type?

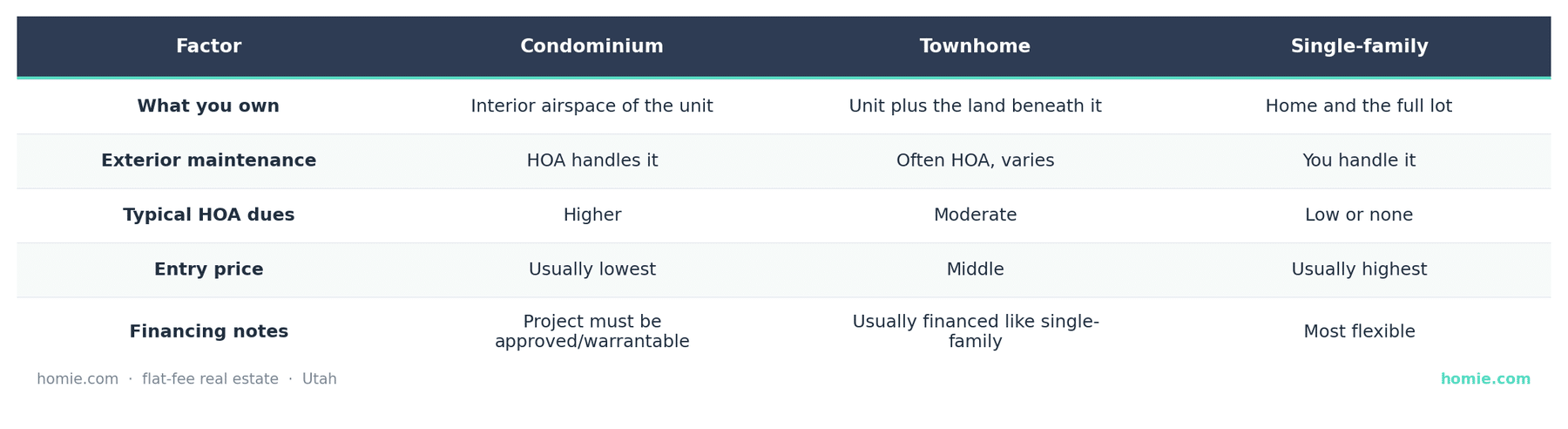

The core difference is what the deed covers. In a single-family home you own the structure and the land it sits on. In a townhome you typically own the unit and the land directly beneath it, often with shared walls and an HOA that maintains common areas. In a condominium you own the interior airspace of your unit while the building, land, and exteriors are owned in common and managed by the association. That ownership line drives almost everything else: who maintains the roof, who carries the master insurance policy, and how much the HOA collects each month.

Ranges and tendencies are general. Read the specific HOA documents and budget for any property before relying on them.

How does financing differ across the three?

A single-family home and most townhomes are financed in a straightforward way, underwritten on you and the property. Condos add a layer: the lender also evaluates the condo project itself. For an FHA or VA loan, the project generally must be approved or “warrantable,” meaning it meets standards for owner-occupancy ratios, the share of units one entity can own, the reserve fund, and the percentage of dues that are delinquent. This matters for first-time buyers because a condo in a non-warrantable project can be harder to finance with a low-down-payment loan, which narrows your future buyer pool too. Before you fall for a specific condo, ask whether the project is FHA-approved or conventionally warrantable, and confirm it with your lender. Townhomes structured as planned-unit developments usually avoid this hurdle and finance much like single-family homes.

What can a Utah HOA actually charge and control?

If the home is in an HOA, Utah’s Community Association Act (Title 57, Chapter 8a for community associations, with condominiums also governed under Title 57, Chapter 8) sets the framework for what the association can do. Associations can levy regular dues, special assessments for major repairs, and fines for rule violations, and they must follow the statute’s procedures for budgets, reserves, notice, and enforcement. Three things to read before you buy into any Utah HOA:

- The budget and reserves: A thin reserve fund signals future special assessments. Healthy reserves mean the roof and parking lot are already being funded.

- The CC&Rs and rules: These govern rentals, pets, parking, and exterior changes. Rental caps in particular can matter if you ever want to lease the home.

- The resale or estoppel disclosures: Utah associations provide records on dues, pending assessments, and litigation. Read them during your due-diligence window.

A low monthly due with no reserves can cost more over five years than a higher due that keeps the community funded. Look at the whole picture, not just the headline number.

How do the three compare on resale and appreciation?

All three appreciate with the broader Wasatch Front market, but they do not move identically. Single-family homes generally show the widest buyer pool and the steadiest demand, because they appeal to the most households and are the easiest to finance. Townhomes have broadened in appeal as entry prices rose, drawing first-time buyers and downsizers who want low maintenance without condo-style shared ownership. Condos offer the lowest entry price and can be the fastest path into ownership, but their resale can be more sensitive to the project’s financing status and HOA health. The practical takeaway for a first-time buyer: a condo or townhome can be the smartest way into the market at today’s prices, as long as you vet the HOA and the project’s financeability as carefully as you vet the unit itself.

Frequently Asked Questions

What is the difference between a condo and a townhome in Utah?

In a condo you own the interior airspace of your unit while the building and land are owned in common; in a townhome you typically own the unit and the land beneath it. Condos usually carry higher HOA dues because the association maintains more, and condos can face extra financing requirements.

Why are some Utah condos harder to finance?

Low-down-payment loans like FHA and VA generally require the condo project to be approved or warrantable, based on owner-occupancy, reserves, delinquency, and single-owner concentration. A non-warrantable project narrows financing options for you and future buyers, so confirm the project’s status with your lender.

What can a Utah HOA charge me?

Under Utah’s Community Association Act, an HOA can levy regular dues, special assessments for major repairs, and fines for rule violations, following the statute’s notice and budget procedures. Read the budget, reserves, CC&Rs, and resale disclosures before buying.

Is a townhome a good first home in Utah?

For many first-time Utah buyers, yes. Townhomes often sit between condos and single-family homes on price and maintenance, usually finance like single-family homes, and have a broad resale audience. The key is vetting the HOA’s health before you commit.

Which holds value best in Utah, a condo, townhome, or house?

Single-family homes generally have the widest buyer pool and steadiest demand, while townhomes have broadened in appeal and condos offer the lowest entry but can be more sensitive to HOA and financing status. All three track the broader market; the property type mainly affects how easily it resells.

That’s the three-way breakdown. If you’re buying your first Utah home and want a brokerage that will read the HOA budget and check a condo’s financeability with you before you write, homie.com/buy is where we work. None of the above is legal or lending advice, so confirm HOA rules and loan eligibility for any specific property before you commit.

— The Homie Team

- Utah Community Association Act, Title 57 Chapter 8a

- Utah Condominium Ownership Act, Title 57 Chapter 8

- HUD/FHA condominium project approval

- Consumer Financial Protection Bureau, loan options

*All brokerage fees, including listing and buyer agent compensation, are fully negotiable and determined solely by the seller and service provider. *Flat-fee pricing and service availability may vary by location and are subject to change over time. Verify current pricing before listing. *Past performance is not indicative of future results. *Examples and potential savings are for illustrative purposes only.