In a market that still moves quickly along much of the Wasatch Front, a mortgage pre-approval is the difference between making a credible offer and watching the home go to someone who already had their financing lined up. Most national guides explain the mechanics, but they skip how the steps connect to Utah’s market timing and what a Utah listing agent actually expects to see clipped to your offer. This walkthrough covers the full path: the difference between pre-qualification and pre-approval, the documents a lender will ask for, how long the letter lasts, and how rate locks work. This is general guidance, not lending advice. Your lender sets the specifics for your situation.

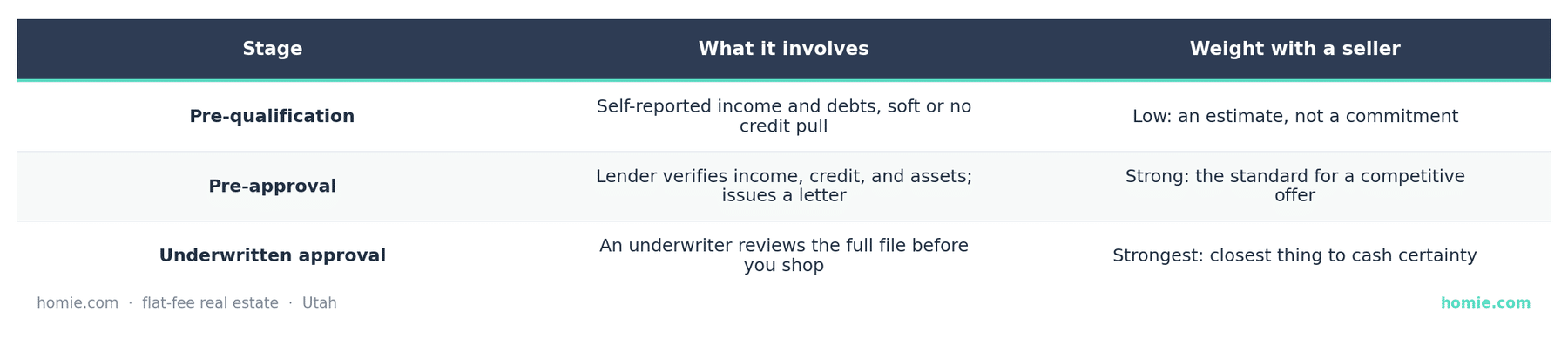

Pre-qualification vs. pre-approval vs. underwritten approval: what’s the difference?

These three terms get used interchangeably, but they carry very different weight with a Utah seller. A pre-qualification is a quick estimate based on numbers you state; a pre-approval is a lender’s conditional commitment after reviewing your actual documents and credit; an underwritten (or “fully underwritten”) approval goes a step further, with an underwriter signing off before you even have a property.

In a competitive Utah market, a pre-approval is the practical minimum, and an underwritten approval can set your offer apart when listings draw multiple bids.

What documents does a Utah lender ask for?

A lender verifies three things: your income, your assets, and your credit. Have these ready before you apply and the process moves in days rather than weeks.

- Income: Recent pay stubs, the last two years of W-2s or 1099s, and tax returns if you are self-employed or commissioned.

- Assets: Recent bank and investment statements showing your down payment and reserves, plus documentation for any large or gifted deposits.

- Identity and debts: Government ID, and authorization for the lender to pull your credit and review existing obligations.

The lender uses these to calculate your debt-to-income ratio and confirm your down payment is sourced and seasoned. Self-employed buyers and those with variable income should expect more documentation and a little more time.

What does the pre-approval process look like step by step?

The path is consistent whether you use a local Utah lender or a national one.

- Step 1: Check your own credit and fix obvious errors before you apply, since the score drives both approval and rate.

- Step 2: Gather the income, asset, and identity documents above.

- Step 3: Apply with one or more lenders and authorize the credit pull. Shopping several lenders within a short window is generally treated as a single inquiry for scoring purposes.

- Step 4: Review the loan estimate each lender provides, comparing rate, fees, and program, not just the monthly payment.

- Step 5: Receive your pre-approval letter, then shop for homes inside that budget.

A Utah listing agent will look for a pre-approval letter that matches or exceeds your offer price and comes from a reputable lender. Getting the letter before you tour homes keeps you ready to write when the right one appears.

How long does a pre-approval last, and how do rate locks work?

A pre-approval letter is typically valid for a set window, often around 60 to 90 days, after which the lender refreshes your credit and documents because both can change. If your search runs long, expect to update the letter. The pre-approval is about qualifying for the loan; it is not the same as locking your interest rate. A rate lock holds a specific interest rate for a defined period while you move toward closing, protecting you if rates rise during that window. Locks are usually tied to a property and a timeline, so you generally lock after you are under contract, not at the pre-approval stage. Ask your lender how long their locks run, what extensions cost, and what happens if your closing slips.

Local lender or national lender?

Both can get you to the closing table, and the right answer depends on service and terms, not geography. A local Utah lender or credit union may know the market and the timelines well and can sometimes turn files around quickly, which matters when an offer hinges on a fast pre-approval. A national lender may compete hard on rate and fees. The way to choose is to compare loan estimates side by side, weigh responsiveness, and ask your agent who has actually performed on recent Utah closings.

Frequently Asked Questions

Do I need a pre-approval before making an offer in Utah?

Practically, yes. In most competitive Utah markets a seller expects a pre-approval letter with the offer, and many listing agents will not present an offer without one. Cash buyers substitute proof of funds.

How long does mortgage pre-approval take in Utah?

If your documents are ready, a pre-approval can often be issued within a few business days. Self-employment, variable income, or gift funds can extend the timeline because they require more verification.

Does getting pre-approved hurt my credit score?

A pre-approval involves a hard credit inquiry, which can have a small, temporary effect. Shopping multiple mortgage lenders within a short window is generally counted as a single inquiry for scoring, so comparing lenders does not stack up the impact.

How long is a Utah pre-approval letter good for?

Pre-approval letters are typically valid for roughly 60 to 90 days, after which the lender refreshes your credit and documents. If your home search runs longer, ask your lender to update the letter.

Is a pre-approval the same as a locked interest rate?

No. A pre-approval qualifies you for a loan amount; a rate lock holds a specific interest rate for a set period and is usually done after you are under contract on a specific home. Ask your lender how their locks and extensions work.

That’s the path from “thinking about it” to “ready to write.” If you’re buying in Utah and want a brokerage that will line your pre-approval up with the offer and watch the deadlines with you, homie.com/buy is where we work. None of the above is lending or legal advice, so let your lender confirm the numbers and terms for your situation before you commit.

— The Homie Team

- Consumer Financial Protection Bureau, mortgage guidance

- CFPB, Loan Estimate explainer

- Fannie Mae, homebuyer education and eligibility

- Utah Division of Real Estate, consumer resources

*All brokerage fees, including listing and buyer agent compensation, are fully negotiable and determined solely by the seller and service provider. *Flat-fee pricing and service availability may vary by location and are subject to change over time. Verify current pricing before listing. *Past performance is not indicative of future results. *Examples and potential savings are for illustrative purposes only.